JAV rinkos rodo prieštaringus ženklus, todėl prognozuoti sunku. Pagrindinis priešinis vėjas – infliacija – mažėja, tačiau darbo rinka stipri, mažėja nedarbas, auga atlyginimai. Federalinis rezervų bankas padidino palūkanų normas sparčiausiai nuo devintojo dešimtmečio, padidindamas jas nuo beveik nulio iki daugiau nei 1980% per pastaruosius 5 mėnesių, rizikuodamas nuosmukiu, bandydamas išlaikyti kainų ribą.

Bet ar Fed pastangos nueis į niekais? Palūkanų normos didėjimas paprastai daro įtaką rinkoms su 12–18 mėnesių vėlavimu, o dabar matome, kad infliacija mažėja – paskutiniai balandžio mėnesio duomenys rodė 4.9 % metinį augimo tempą, gerokai mažiau nei pernai buvo 9.1 %. viršūnė. Tačiau šis 4.9% vis dar yra daugiau nei dvigubai didesnis už FED tikslinę normą.

Tai yra pagrindas naujausiems Goldman Sachs vadovo Davido Solomono komentarams, kurie mano, kad infliacija vis dar yra didelis iššūkis ekonomikai.

„Jaučiu, kad jis bus lipnesnis, pasiekė aukščiausią tašką, bet bus lipnesnis ir atsparesnis, todėl tikimės, kad nors Fed gali pristabdyti ir priklausys nuo duomenų, jums gali prireikti tarifus, kad galų gale jį dar labiau kontroliuotų“, – teigė Solomonas.

Tokioje klampioje infliacinėje aplinkoje investuotojai natūraliai pereis prie gynybinių akcijų – tų, kurios gali parodyti atsparumą nuosmukiui. Naudodami „TipRanks“ platformą, surinkome informaciją apie du pavadinimus, kuriuos „Goldman Sachs“ analitikai rekomenduoja kaip gynybines akcijas. Čia yra detalės.

„Flywire Corporation“. (FLYW)

Pirmiausia mūsų sąraše yra „Flywire“, internetinė mokėjimų apdorojimo paslauga. Pradėdama kaip švietimo sektoriaus specialistė, įmonė patraukė įdomiu keliu į perpildytą mokėjimų internetu nišą. Nuo tada ji išplėtė savo paslaugas, įtraukdama mokėjimų apdorojimą pasauliniame tinkle, aprūpindama sveikatos priežiūros, kelionių ir B2B pramonės šakas, be švietimo. „Flywire“ yra pritaikyta patenkinti klientų tikrinimo ir saugumo atitikties poreikius, veikianti daugiau nei 140 valiutų.

„Flywire“ gali pasigirti tikrai pasauliniu pasiekiamumu, turėdama daugiau nei 3,300 verslo klientų 240 šalių ir teritorijų. Bendrovė siūlo paslaugas ir palaikymą dešimtimis kalbų visą parą, todėl mokėjimo procesas vyksta sklandžiai iš bet kokios perspektyvos. Be pagrindinių pavadinimų, tokių kaip „Mastercard“, „Visa“ ir „AMEX“, „Flywire“ taip pat bendradarbiauja su „PayPal“ ir „Venmo“.

Kaip gynybinė akcija, „Flywire“ turi naudos iš pasaulinio perėjimo prie skaitmeninių operacijų ir biuro be popieriaus. Įvairaus masto įmonės, nuo mažiausių „Mom & Pop“ parduotuvių iki pramonės gigantų, tokių kaip „Mastercard“, gali padidinti efektyvumą pereidamos nuo popierinių operacijų prie skaitmeninio apdorojimo. Būdamas elektroninių mokėjimų specialistas, Flywire yra patogiai išdėstytas tinkamu laiku ir tinkamoje vietoje. Bendrovės akcijos šiais metais pabrango maždaug 21%, o tai gerokai viršijo S&P 500 8% prieaugį per metus. Turėdama aiškių požymių, kad skaitmeninių mokėjimų sektorius nuolat plečiasi, „Flywire“ yra tvirtai pasirengęs išlaikyti savo augimą kartu su savo klientų baze.

Pagrindinis bendrovės 1-iojo ketvirčio finansinio pranešimo rezultatas pasakoja istoriją: „Flywire“ aukščiausios linijos pajamos per metus išaugo 23% ir pasiekė 46 mln. USD – ir tai viršijo prognozes beveik 94.4 mln. USD. Kaip ir daugelis technologijų įmonių, „Flywire“ patiria grynųjų nuostolių, tačiau jos pirmojo ketvirčio EPS nuostolis yra 11.48 centai, palyginti su 1 centų už akciją nuostoliu prieš metų ketvirtį – ir tai buvo 3 centais už akciją geriau, nei tikėtasi. „Flywire“ pakoreguotas EBITDA skaičius per metus smarkiai išaugo – nuo 10 mln. USD iki 4 mln. Pagrindiniai „Flywire“ pirmojo ketvirčio įvykiai buvo 1.9 naujų klientų, todėl 7Q170 buvo didžiausias visų laikų bendrovės pardavimų ketvirtis.

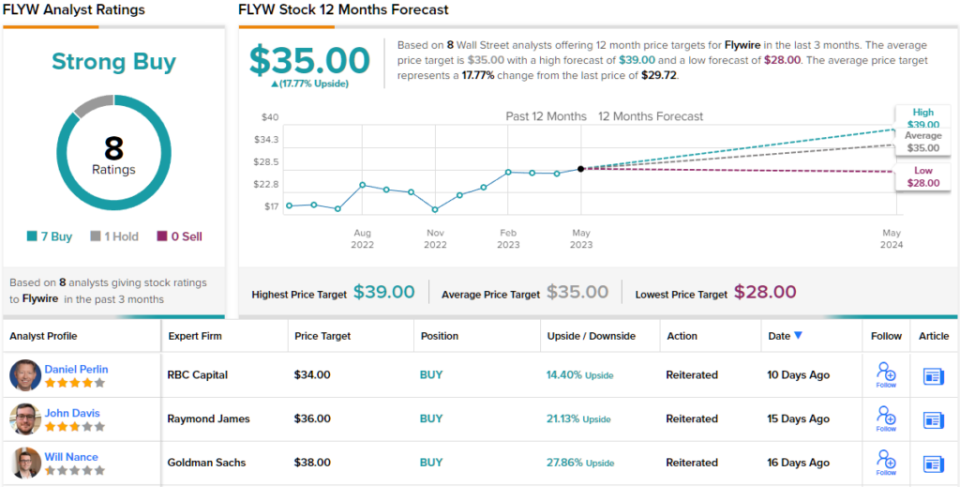

„Goldman Sachs“ pagrindiniai dalykai yra stipri „Flywire“ gynybinė bazė ir jos gebėjimas skatinti augimą šiandieninėje ekonomikoje. Analitikas Willas Nance'as rašo: „Žvelgdami į ateitį, manome, kad stiprūs FLYW NRR rezultatai, kartu su įsipareigojimu užtikrinti nuoseklų veiklos svertą, turėtų padėti bendrovei ir artimiausiu metu tęsti geresnius rezultatus. Visų pirma, matome, kad įmonės gynybinis verslo derinys švietimo ir sveikatos priežiūros srityse yra tinkamas, kad likusią šių metų dalį galėtų absorbuoti makroekonominio silpnumo potencialą.

„Sudėjus, – apibendrino analitikas, – kai akcijomis prekiaujama 47 kartus daugiau nei 2024 m. EBITDA, manome, kad vertinimas yra patrauklus atsižvelgiant į FLYW ~30–40 % augimo tempus, įspūdingą normos maržos padidėjimą ir tvarumą. jos stiprios NRR, nes pastarųjų metų rekordinės grupės ir toliau auga.

Atsižvelgdama į tai, Nance suteikia FLYW akcijų pirkimo reitingą su 38 USD tiksline kaina, o tai reiškia, kad ateinančiais metais gali padidėti ~28%. (Norėdami pamatyti Nance'o įrašą, spustelėkite čia)

„Goldman“ variantas vargu ar yra išskirtinis. Iš 8 naujausių analitikų apžvalgų yra aiškus suskirstymas nuo 7 iki 1, o ne pirkimo rekomendacijos, o ne sulaikymai, o tai rodo stiprų pirkimo konsensuso įvertinimą. Šiuo metu akcijų kaina yra 29.72 USD, o vidutinė tikslinė kaina yra 35 USD, o tai rodo, kad per 12 mėnesių jis padidės maždaug 18%. (Matyti FLYW atsargų prognozė)

Walmart, Inc. (WMT)

Dabar mes perkelsime savo dėmesį nuo pažangiausių „fintech“ į vieną iš tradiciškiausių mažmenininkų: „Walmart“. Iš savo kuklių Arkanzaso šaknų išaugęs „Walmart“ pagal pajamas tapo didžiausia pasaulyje mažmeninės prekybos milžine, 611 finansiniais metais (apimant 2023 mėnesių, pasibaigiančių šių kalendorinių metų sausio 12 d.) uždirbusia daugiau nei 31 mlrd. Įmonei priklauso ir „Walmart“, ir „Sam's Club“ mažmeninės prekybos tinklai, valdantys platų supercentrų, nuolaidų universalinių parduotuvių ir bakalėjos parduotuvių asortimentą JAV ir tarptautiniu mastu. Iš viso „Walmart“ turi daugiau nei 10,500 24 parduotuvių 46 šalyse ir veikia XNUMX skirtingais pavadinimais.

„Walmart“ neseniai paskelbė savo 2024 finansinių metų pirmojo ketvirčio finansinius rezultatus ir parodė, kad išlaiko augimo trajektoriją. Bendrovė pranešė, kad bendros ketvirčio pajamos siekė 152.3 mlrd. USD, ty 7.6% daugiau nei per metus ir 4.39 mlrd. USD viršija prognozes. Bendrovės ne GAAP EPS rodiklis 1.47 USD buvo 15 centų geresnis nei tikėtasi.

Tarp rezultatų išryškėjo JAV kompanijų pardavimai, kurie per metus išaugo 7.4 %; elektroninė prekyba, kuri išaugo įspūdingai 27%; ir pasaulinis reklamos verslas, kuris per metus išaugo 30 %.

Taip pat per pirmąjį fiskalinį ketvirtį „Walmart“ savo akcininkams grąžino 1 mlrd. Didelė dalis to buvo sumokėta iš bendrovės dividendų, kurie paskutinį kartą buvo paskelbti 2.2 centais už paprastąją akciją, išmokėti gegužės 57 d. Nors metinė 30 USD už akciją norma suteikia nedidelį, tik 2.28 proc. pelną, investuotojai turėtų atkreipti dėmesį į dividendų dydį. patikimumas: „Walmart“ moka dividendus nuo 1.54 m., nepraleido nė ketvirčio ir kasmet didina mokėjimą.

Be savo klasikinio gynybinio dividendų mokėjimo, Walmart akcijos parodė gebėjimą augti net ir esant stipriam priešpriešiniam vėjui.

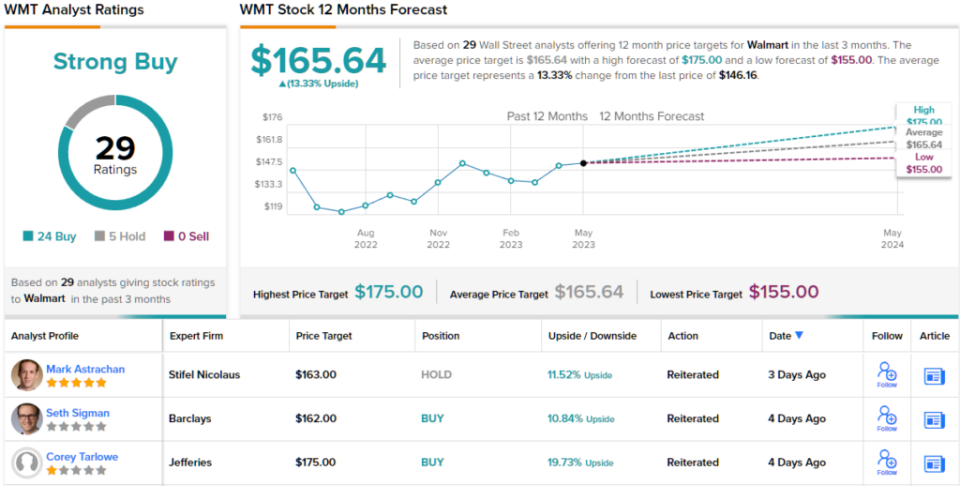

Nė vienas iš šių dalykų nepastebėjo Goldman analitės Kate McShane, kuri apie Walmart sako: „Manome, kad WMT yra akcijos, kurias investuotojai vis dar nori turėti, atsižvelgiant į jos gynybines savybes artimiausiu metu ir gerėjantį pelningumo profilį ilguoju laikotarpiu. “

Šiuo tikslu 5 žvaigždučių analitikė vertina WMT akcijų pirkimą, o jos tikslinė kaina, nustatyta 176 USD, rodo, kad ateinančiais metais akcijos augs 20%. (Jei norite pamatyti McShane įrašą, spustelėkite čia)

Didžiausi Wall Street vardai niekada nestokoja analitikų susidomėjimo, o „Walmart“ nėra išimtis. Akcijos sulaukė 29 naujausių analitikų apžvalgų, įskaitant 24 pirkimus ir tik 5 sulaikymus, kad būtų pasiektas „Strong Buy“ konsensuso reitingas. „Walmart“ akcijomis šiuo metu prekiaujama 146.16 USD, o vidutinė tikslinė kaina yra 165.64 USD, o tai reiškia 13% prieaugį per vienerius metus. (Matyti WMT akcijų prognozė)

Norėdami rasti gerų idėjų, kaip prekiauti akcijomis patraukliais vertinimais, apsilankykite „TipRanks“ geriausios akcijos, kurią galima nusipirkti – įrankį, kuris sujungia visas „TipRanks“ akcijų įžvalgas.

Atsakomybės neigimas: Šiame straipsnyje pareikštos nuomonės yra tik analizuojamų analitikų nuomonės. Turinį ketinama naudoti tik informaciniais tikslais. Prieš investuodami, labai svarbu atlikti savo analizę.

Šaltinis: https://finance.yahoo.com/news/david-solomon-warns-inflation-stickier-004127652.html